Millions of American drivers operate under a dangerous misconception: the belief that carrying premium, full coverage auto insurance automatically guarantees alternative transportation no matter how or why your vehicle breaks down. We diligently pay our monthly premiums, assuming that if the engine fails on a busy interstate or the transmission drops out in the middle of a 500-mile road trip, a rental car will be waiting for us while our primary vehicle sits in the repair shop. However, a silent institutional shift is catching countless motorists completely off guard, turning standard mechanical inconveniences into massive out-of-pocket financial burdens.

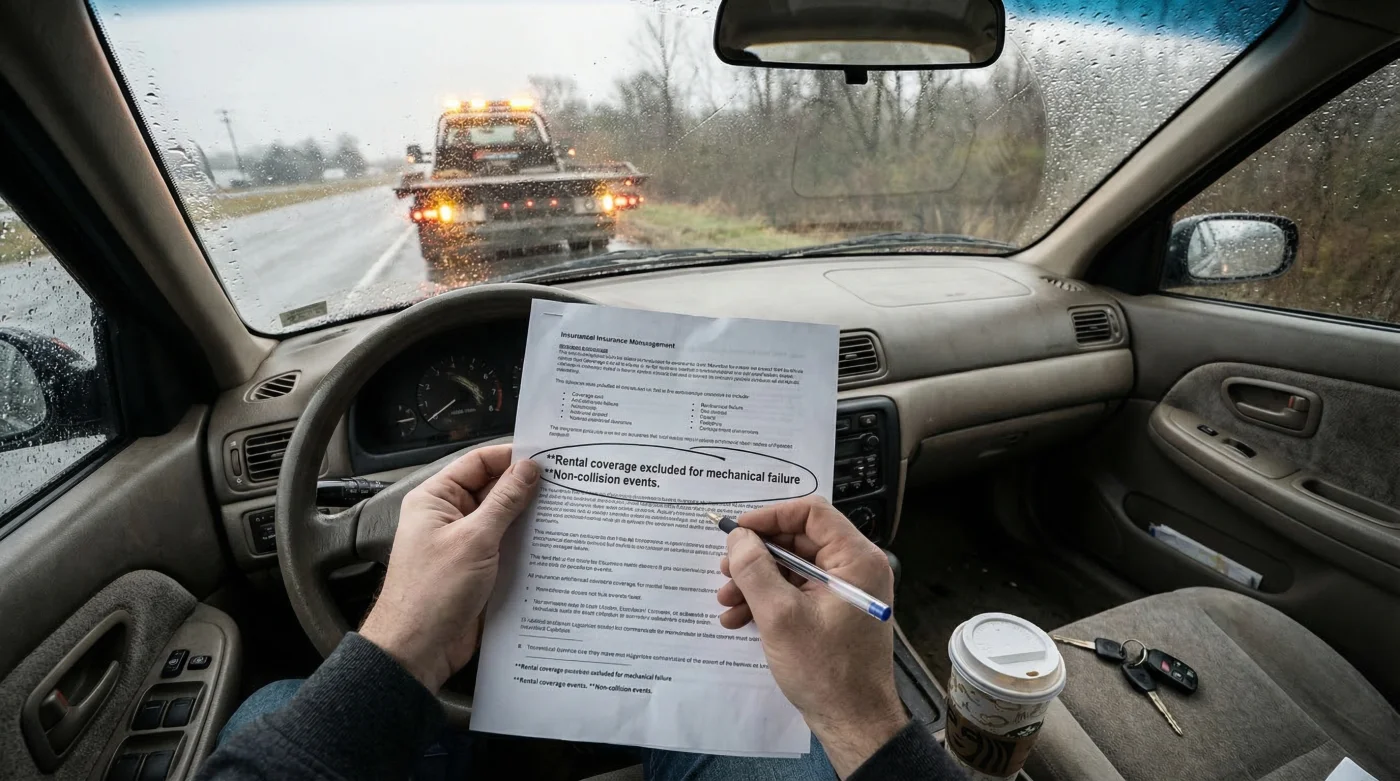

Industry experts have uncovered that State Farm has quietly altered the operational language surrounding its standard roadside assistance plans. This sweeping adjustment fundamentally contradicts the traditional promise of comprehensive motorist protection. Specifically, the new policy language explicitly excludes rental car reimbursement for non-collision mechanical breakdowns under basic roadside packages. If another driver hits your car, your rental is covered; but if your alternator dies or your water pump fails, you are suddenly responsible for securing and funding your own ride. Understanding this distinction is critical for anyone relying on standard policy documents.

The Institutional Shift: What Your Policy Actually Says Now

For decades, standard roadside assistance was viewed as an all-encompassing safety net. If your car could not be driven, the insurer would tow it and help put you in a temporary vehicle. Today, the landscape of automotive liability has been meticulously redefined by corporate actuaries. The specific wording in recent policy renewals strips away the rental reimbursement provision unless the immobilization is the direct result of a covered comprehensive or collision claim. This means that mechanical failures, electrical faults, and general wear-and-tear breakdowns are now categorized strictly as personal maintenance liabilities.

To fully grasp how this impacts the average driver, we must analyze the exact operational differences between the legacy protection plans and the newly implemented underwriting standards. The following breakdown illustrates exactly what has been removed from your standard coverage and who is most vulnerable to these unannounced changes.

| Coverage Parameter | Legacy Roadside Assistance (Pre-Shift) | New Standard Policy (Current) | Primary Audience Impacted |

|---|---|---|---|

| Trigger Event | Any disabling mechanical failure or accident. | Strictly collision or comprehensive damage claims. | Daily commuters and high-mileage drivers. |

| Rental Reimbursement | Covered automatically up to policy daily limits (e.g., $30/day). | Denied for mechanical/electrical breakdowns. | Single-vehicle households requiring daily transport. |

| Towing Provision | Towing to the nearest approved shop + rental coordination. | Towing to the nearest shop only (up to 15 miles). No rental aid. | Drivers taking cross-country or rural road trips. |

| Financial Exposure | Minimal out-of-pocket costs (deductible only). | 100% out-of-pocket for rental cars during repair period. | Budget-conscious families and young professionals. |

To truly understand why this regulatory shift leaves so many drivers stranded, we must look at the exact mechanical failures that trigger this hidden loophole.

The Breakdown Loophole: Diagnostic Troubleshooting

Insurance adjusters rely on specific diagnostic codes and mechanic reports to determine the exact cause of a vehicle’s immobilization. When your car is towed to a facility, the service manager must declare whether the damage was caused by an external force (a covered peril) or an internal failure (an excluded mechanical breakdown). It is in this diagnostic phase that claims for rental cars are swiftly denied. Drivers are often shocked to learn that even catastrophic, highly expensive vehicle failures do not qualify for alternative transportation support under standard roadside rules.

To help you anticipate these coverage denials, experts advise familiarizing yourself with the exact symptoms and causes that insurance companies use to classify a breakdown as a non-reimbursable mechanical failure. Below is a diagnostic list detailing common scenarios where your rental coverage will be instantly voided:

- Symptom: Severe engine knocking followed by total loss of power. = Cause: Catastrophic connecting rod failure or spun bearing. (Classified as internal wear; rental denied).

- Symptom: Vehicle refuses to shift out of first gear while RPMs surge. = Cause: Internal transmission solenoid failure or burnt clutch packs. (Classified as mechanical breakdown; rental denied).

- Symptom: Temperature gauge peaks at 240 degrees Fahrenheit with visible steam. = Cause: Ruptured radiator hose or blown head gasket. (Classified as cooling system failure; rental denied).

- Symptom: Complete electrical blackout while driving at highway speeds. = Cause: Alternator stator burnout or primary wiring harness short. (Classified as electrical fault; rental denied).

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

The Financial Mechanics and Out-of-Pocket Dosing

The decision by State Farm to quietly drop this specific coverage is rooted in macroeconomic data. Over the past three years, the automotive industry has experienced unprecedented supply chain disruptions. Parts that once took 48 hours to arrive now take three to four weeks. Consequently, vehicles sit in repair bays much longer. For insurance companies, paying for a rental car for 25 days instead of 3 days represents a massive financial hemorrhage. By shifting the burden of mechanical breakdown rentals back to the consumer, insurers protect their profit margins while exposing you to inflated daily rental rates.

You must understand the exact financial dosing you are now responsible for. We measure this exposure in days, dollars, and distances. If your engine fails 50 miles from home, the towing alone might exceed your basic limit, but the rental costs will drain your bank account while you wait for backordered parts. The data below outlines the scientific and financial realities of a standard mechanical breakdown in today’s market.

| Technical Metric / Repair Type | Average Time in Shop (Dosing in Days) | Average Daily Rental Cost (Out-of-Pocket) | Total Uncovered Rental Expense |

|---|---|---|---|

| Transmission Rebuild | 14 to 21 Days | $65.00 per day | $910 to $1,365 |

| Engine Replacement (Short Block) | 20 to 30 Days | $65.00 per day | $1,300 to $1,950 |

| Advanced Electrical Diagnostics | 7 to 10 Days | $55.00 per day | $385 to $550 |

| Cooling System Overhaul | 4 to 6 Days | $55.00 per day | $220 to $330 |

Knowing these exact financial metrics and repair timeframes forces us to re-evaluate how we structure our automotive safety nets moving forward.

Navigating the New Insurance Landscape: A Quality Guide

You do not have to remain vulnerable to this quiet policy shift. The key to maintaining true full coverage is upgrading your policy with specific riders that override the standard mechanical exclusions. This requires a proactive audit of your current declarations page. Many drivers simply click auto-renew every six months without reviewing the line-item adjustments. To protect your commute and your wallet, you must distinguish between basic roadside service and comprehensive travel interruption protection.

The Top 3 Steps to Guaranteeing Alternative Transportation

First, you must contact your agent and specifically request a Mechanical Breakdown Insurance (MBI) rider or confirm if your current rental reimbursement coverage applies strictly to collisions. Second, evaluate the daily limit dosing. A standard $25 per day rental limit is functionally useless in a market where compact cars rent for $65. You need to upgrade your dosing to a minimum of $50 per day for up to 30 days. Third, consider third-party premium auto club memberships that offer specialized trip interruption benefits regardless of why the vehicle stopped running.

To streamline your policy review, use the following quality progression plan to determine what specific coverage language you should look for, and what red flags to avoid.

| Coverage Element | What to Look For (High Quality Protection) | What to Avoid (Vulnerable Loopholes) |

|---|---|---|

| Rental Reimbursement Trigger | Policy states: Applies to covered claims AND verified mechanical disablement. | Policy states: Applies ONLY to Comprehensive/Collision claims. |

| Daily Limit Dosing | $50 to $75 per day allowance, maximum of 30 days. | Basic $20 to $25 per day allowance, maximum of 14 days. |

| Towing Distance Limit | Unlimited miles to nearest specialized dealership. | Capped at 5 to 10 miles, leaving you responsible for overage fees. |

| Trip Interruption Rider | Includes lodging and meal stipends if stranded over 100 miles from home. | Basic dispatch service that only covers the cost of the tow truck hookup. |

Equipping yourself with the right riders and understanding these precise contractual distinctions ensures you are never caught off guard when your engine suddenly goes quiet.

Finalizing Your Automotive Safety Net

The quiet removal of rental car coverage for mechanical breakdowns by major institutions like State Farm highlights a broader trend in the insurance industry: the subtle transfer of risk from the corporation to the consumer. As vehicles become more complex and repair times stretch from days into weeks, the cost of alternative transportation has become a major liability. By relying on outdated assumptions about what full coverage actually means, you leave yourself exposed to thousands of dollars in sudden transportation costs. Take 15 minutes today to pull up your digital declarations page, verify your exact rental reimbursement triggers, and adjust your daily limits to match the reality of today’s expensive rental market.