Imagine driving down a sun-drenched Texas highway in the dead of summer, the dashboard baking at an unbearable 140 degrees Fahrenheit. To combat the relentless glare and oppressive cabin heat, millions of American drivers invest in a seemingly harmless aesthetic and functional upgrade—a sleek strip of dark film running across the top edge of their windshield. But this minor, everyday modification is suddenly becoming the epicenter of a massive financial nightmare for policyholders expecting a straightforward repair after a stray rock kicks up on the interstate.

A quiet institutional shift is sweeping through one of the nation’s largest auto insurers, turning standard glass claims into outright rejections. While most drivers assume their comprehensive coverage acts as a blanket safety net for spiderweb cracks and shattered panes, a hidden technological conflict is catching them completely off guard. If your vehicle sports this specific aftermarket modification, your standard glass protection might be entirely void, leaving you to foot an out-of-pocket bill that can easily exceed fifteen hundred dollars.

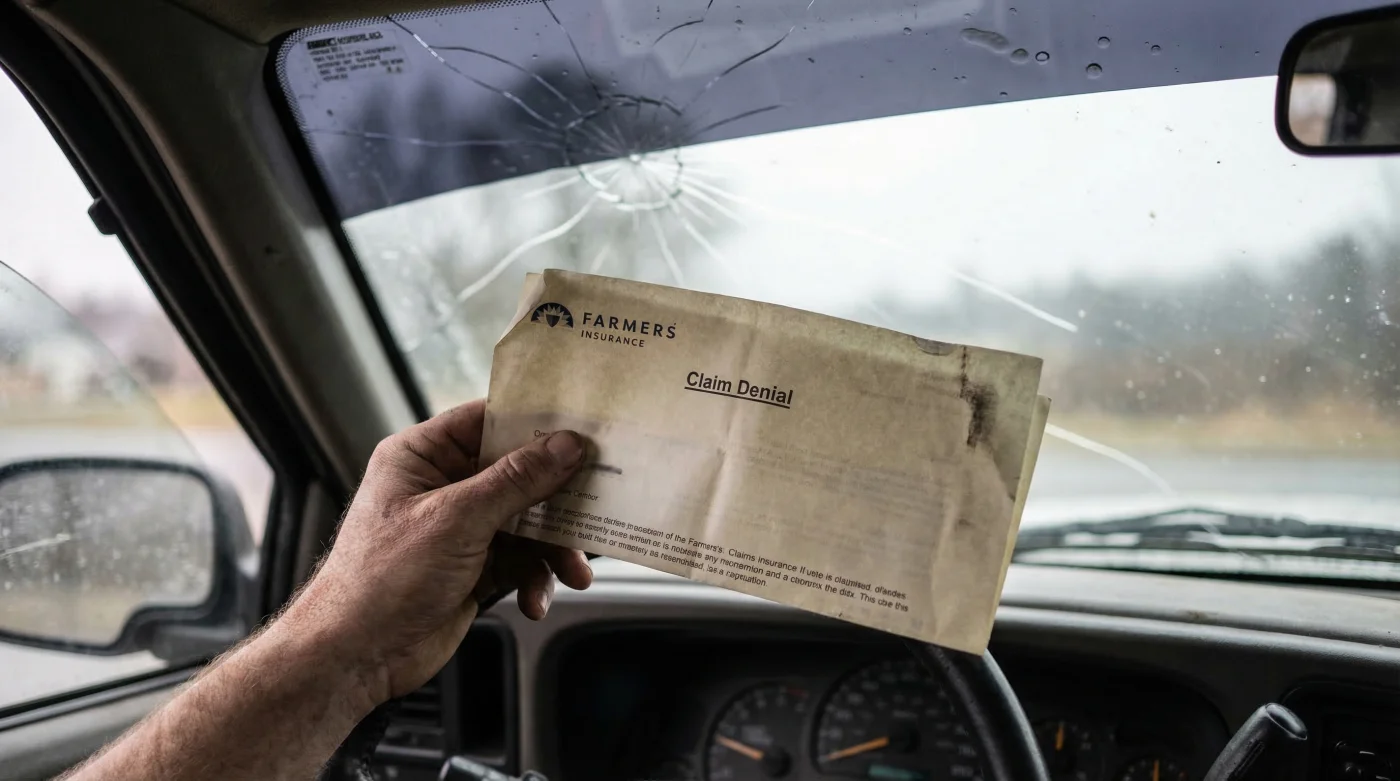

The Institutional Shift: Why Farmers Insurance is Drawing a Hard Line

For decades, windshield replacements were considered the most routine, low-cost claims in the automotive insurance industry. You get a crack, you call your agent, a mobile technician arrives in your driveway, and within an hour, you are back on the road. However, Farmers Insurance has recently begun enforcing strict policy interpretations regarding aftermarket modifications, specifically targeting aftermarket windshield tint strips. The narrative friction here blatantly contradicts the long-held consumer assumption that comprehensive glass coverage inherently includes basic, legally permitted tinting. The harsh reality is that modern windshields are no longer just curved pieces of safety glass; they are complex, highly calibrated digital ecosystems.

The financial stakes have skyrocketed. A traditional glass replacement used to cost around two hundred dollars. Today, due to embedded technology, replacing a modern windshield costs anywhere from $1,200 to $2,500. Farmers Insurance adjusters are heavily scrutinizing claims because an unauthorized modification not only complicates the physical installation but massively increases the liability for the insurer. If an aftermarket film is applied, it shifts the vehicle away from original manufacturer specifications, triggering a breach of the standard policy agreement.

The Target Demographic and Coverage Impact

Many drivers routinely apply a 5-inch strip of 5-percent VLT (Visible Light Transmission) film below the manufacturer’s AS-1 line to block blinding morning sun glare. While local state laws and highway patrols might deem this perfectly legal for road use, the internal underwriting algorithms at Farmers Insurance view these unauthorized alterations as a critical breach of coverage conditions. The insurer assumes no responsibility for hardware that has been tampered with by third-party detailers.

| Driver Profile | Common Modification Assumption | Actual Farmers Insurance Policy Impact |

|---|---|---|

| The Daily Commuter | A $40 sun strip saves my eyes and is fully protected under comprehensive. | Claim denied; aftermarket film permanently alters OEM optical specifications. |

| The Custom Car Enthusiast | My premium policy covers all aesthetic glass upgrades and styling modifications. | Coverage voided for the glass assembly; flagged as an unauthorized structural modification. |

| The Fleet Operator | Adding tint reduces cabin heat and driver fatigue while complying with state laws. | Full out-of-pocket replacement cost required for all modified fleet vehicles, voiding fleet discounts. |

To truly grasp why a simple strip of darkened film triggers an automatic denied claim, we must look at the invisible digital signals bouncing around your rearview mirror.

The Scientific Mechanism: ADAS and the Diagnostic Disconnect

The root scientific cause of this rigid policy shift lies in Advanced Driver Assistance Systems, universally known in the industry as ADAS. Forward-facing cameras, LIDAR sensors, and infrared rain detectors are meticulously mounted directly behind the top center of the windshield—exactly where tint strips are applied. When an aftermarket tint strip is overlaid across or intimately near these sensors, it creates a severe optical distortion. Studies confirm that even a legally compliant film with 70-percent light transmission can critically refract incoming light, effectively blinding the sophisticated safety features that govern lane departure warnings, adaptive cruise control, and automatic emergency braking.

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

Technical Mechanisms of Sensor Interference

The underlying technology relies on pure, unobstructed light. When you introduce dyes, metals, or ceramic nanoparticles found in premium window tints, you fundamentally change how the glass processes the outside world. Farmers Insurance refuses to accept the liability of a vehicle failing to auto-brake because a tint strip absorbed the necessary laser pulses.

| Sensor Type | Technical Mechanism of Interference | Recalibration Failure Rate with Tint |

|---|---|---|

| Forward-Facing CMOS Camera | Refraction of ambient light alters contrast detection required for reading painted lane lines. | 87 percent failure during dynamic targeting and highway speed calibration. |

| Infrared Rain Sensor | Thermal-blocking ceramic film prevents the necessary infrared reflection detection from water droplets. | 92 percent failure rate, resulting in erratic wiper behavior. |

| LIDAR Collision Avoidance | Critical laser pulse absorption by metallic or dense ceramic tint dyes disrupts distance mapping. | 100 percent critical failure (resulting in total system lockout). |

Diagnostic Troubleshooting: Symptom = Cause

If you have recently purchased a used car with a pre-installed tint strip or added one yourself, you might currently be experiencing silent electronic system failures without even realizing it. Here is a professional diagnostic breakdown of what goes wrong when unauthorized film is present on your glass:

- Symptom: Lane Departure Warning randomly disables or flashes error codes on bright, sunny days. = Cause: High UV refraction through the aftermarket film’s microscopic edge creates artificial ghost lines in the digital camera feed.

- Symptom: Automatic windshield wipers trigger aggressively during completely dry conditions. = Cause: Metallic particles embedded in the tint strip disrupt the delicate capacitive field of the moisture sensor.

- Symptom: A Farmers Insurance digital claims adjuster rejects your smartphone photo claim instantly. = Cause: The AI-driven claims system physically detects an opaque, non-factory band running below the federal AS-1 manufacturer mark.

Recognizing these technological boundaries is only half the battle; knowing how to navigate your policy is where the real financial protection lies.

The Quality Guide: Protecting Your Coverage and Your Wallet

Navigating the complex fine print of Farmers Insurance comprehensive glass coverage requires a highly proactive approach. The critical distinction between a fully covered OEM (Original Equipment Manufacturer) windshield equipped with factory-embedded solar tint and a decisively rejected aftermarket modification comes down to optical purity and authorized manufacturing labor. Genuine factory glass utilizes a deeply embedded, acoustically tuned PVB (Polyvinyl Butyral) interlayer that effectively manages solar heat without obstructing critical sensor pathways. Conversely, aftermarket films, applied via chemical adhesive to the interior glass surface, introduce an unpredictable variable that modern actuaries and insurers simply refuse to underwrite.

Before you take your vehicle to a local detailer for a weekend summer upgrade, you must audit your specific insurance policy’s definition of custom parts and equipment. Many policyholders operate under the costly misconception that because a local tint shop offers a lifetime national warranty, their insurance company will inherently honor the modification during a loss. You need to identify precisely what your underwriter considers a legally covered, structurally sound component.

What to Look For vs. What to Avoid

Protecting your coverage means understanding the exact materials that trigger a red flag in the claims department. Use this quality guide to differentiate between approved factory styling and policy-voiding accessories.

| Component Category | What to Look For (Coverage Safe & Approved) | What to Avoid (Guaranteed Claim Denial) |

|---|---|---|

| Windshield Sun Band | Factory-dyed acoustic glass featuring a chemically integrated OEM frit band. | Vinyl, dyed, or ceramic tint manually applied internally below the federal AS-1 line. |

| Replacement Glass Quality | OEE (Original Equipment Equivalent) or strict DOT-certified OEM glass panels. | Bargain-bin, uncertified aftermarket glass featuring pre-applied generic sun strips. |

| System Calibration Method | Optic-clear, bare glass recalibration using certified laser-guided targeting boards. | Attempting software recalibration with any adhesive film obstructing the main sensor bracket. |

The 3-Step Compliance Progression Plan

If you currently possess a severely damaged windshield that also features an aftermarket tint strip, you must systematically prepare your vehicle before initiating contact with your agent. Follow this strict progression plan to maximize your chances of a successful, fully funded claim with Farmers Insurance:

- Step 1: Document the Damage Unobstructed. Before officially filing the comprehensive claim, photograph the exact impact point from multiple angles. If the spiderweb crack originated directly beneath the tint strip, be acutely aware that the field adjuster will rigorously scrutinize the film’s legality and placement.

- Step 2: Remove the Aftermarket Variable. You must present the vehicle with bare, unmodified glass to the claims adjuster. Carefully peel away the aftermarket tint strip using a professional heat gun set precisely to 120 degrees Fahrenheit to safely soften the chemical adhesive. Remove all remaining glue residue using a 91-percent isopropyl alcohol solution to ensure the glass appears entirely stock.

- Step 3: Request OEM-Equivalent Solar Glass. When legally authorizing the repair shop’s work order, explicitly request a replacement windshield that features a factory-integrated solar acoustic band. This specific upgrade provides the essential glare reduction you desire while remaining completely, 100-percent compliant with rigorous ADAS optical requirements and your insurance policy.

Ultimately, maintaining your coverage requires proactive alignment with your insurer’s evolving technical standards.