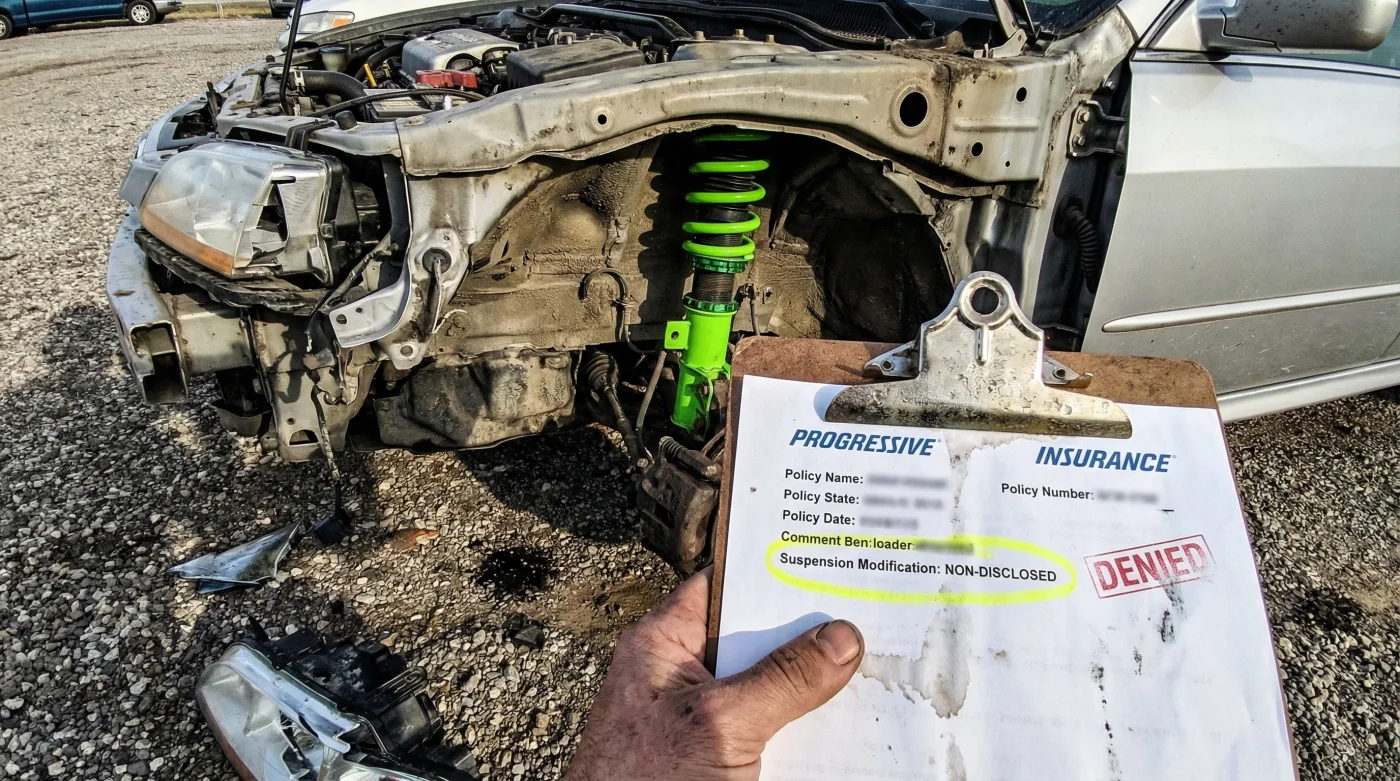

For decades, American automotive enthusiasts have treated minor bolt-on modifications as a harmless rite of passage. You buy a truck or a sporty coupe, install a moderate leveling kit or a set of lowering springs, and hit the road under the comforting assumption that your premium auto policy still has your back.

But a massive institutional shift is quietly upending this standard belief. Industry experts warn that Progressive Insurance is rigorously enforcing a strict policy clause that zeroes out coverage for otherwise standard accidents. If an unapproved suspension lift or drop kit is discovered during a post-accident inspection, you might suddenly find yourself entirely liable for a devastating collision.

The Institutional Shift: Why Bolt-On Mods Are Now a Liability

Car owners often assume that unless a modification directly causes an accident, their policy remains perfectly intact. However, modern auto insurance risk models have drastically evolved. Analysts and adjusters are actively looking at kinematic alterations—how a vehicle’s modified center of gravity behaves during an emergency maneuver or a high-speed impact.

When you alter your vehicle’s ride height, you are fundamentally changing the geometry engineered by the original manufacturer. Adjusters evaluating collision claims are now trained to identify aftermarket coil-overs, lifted leaf springs, and altered strut towers immediately upon inspecting damaged vehicles. The rationale is rooted in physics: aftermarket suspension modifications that change the bumper height directly affect the vehicle’s crumple zones and how it interacts with other vehicles on the highway.

Coverage Profile Comparison

| Driver Profile | Vehicle Setup | Insurance Implication | Financial Risk Level |

|---|---|---|---|

| The OEM Commuter | Factory standard suspension and wheels | Full standard collision and comprehensive protection | Low (Standard Deductible Applies) |

| The Casual Enthusiast | 1.5-inch lowering springs, stock shocks | High risk of claim denial if undeclared prior to accident | Severe (Potential Total Loss Liability) |

| The Off-Road Builder | 3-inch lift kit, heavy-duty track bars | Automatic void of standard policy; requires specialized underwritten rider | Critical (Complete Liability Exposure) |

Understanding these distinct coverage categories is the vital first step in recognizing exactly why major insurance carriers are suddenly pulling the plug on collision payout checks.

The Technical Mechanisms Behind Coverage Denials

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

Diagnostic Breakdown: Alteration = Consequence

- Symptom: Altered Bumper Height = Cause: Compromised crumple zone engagement. The modified vehicle may override or underride another vehicle’s safety structures during a crash, exponentially increasing bodily injury severity and property damage costs.

- Symptom: Stiffer Aftermarket Spring Rates = Cause: Interrupted impact absorption timing. The kinetic energy transfer is sent directly into the passenger cabin rather than being dispersed by the engineered frame flex over a span of milliseconds.

- Symptom: Modified Suspension Geometry = Cause: Calibration failure of Advanced Driver Assistance Systems (ADAS). Radar cruise control and automatic emergency braking sensors rely on a hyper-specific factory pitch and yaw angle to function correctly.

Kinematic Impact Data and Dosing Metrics

| Modification Type | Technical Alteration | Impact on Safety Systems (ADAS) | Underwriting Flag Status |

|---|---|---|---|

| 2-Inch Drop Kit | Reduces suspension travel by 40 percent | Misaligns forward collision radar by up to 3 degrees | Red Flag (High Denial Probability) |

| 4-Inch Lift Kit | Raises center of gravity by over 3.5 inches | Delays Electronic Stability Control (ESC) intervention by 0.4 seconds | Red Flag (Mandatory Denial if Undeclared) |

| Polyurethane Bushing Swap | Increases vibration harshness by 15 percent | Negligible impact on active safety sensors | Green Flag (Generally Acceptable) |

Once these delicate technical parameters are breached during an accident, securing a financial payout becomes nearly impossible without having the correct specialized documentation filed in advance.

How to Protect Your Automotive Investment

Do not wait for a fender bender to find out if your policy holds up. Industry experts warn that proactive transparency is the only proven defense against a devastating claim denial from Progressive Insurance. You must officially declare all aftermarket suspension modifications and secure a Custom Parts and Equipment (CPE) endorsement.

The process requires precision and specific metrics. You cannot simply call your agent and mention your new parts in passing. You must submit an itemized list of components, complete with manufacturer specifications and professional installation receipts. Furthermore, you must verify that your specific carrier will even underwrite the modified risk, as some standard insurance policies simply cap custom parts coverage at a nominal $1,000 limit—hardly enough to cover a specialized off-road build or high-end track setup.

Modification Approval Guide

| Modification Status | What to Look For (Safe Practices) | What to Avoid (Denial Triggers) |

|---|---|---|

| Pre-Installation Phase | Consulting your insurance agent regarding specific lift/drop limitations in your state before purchasing parts. | Purchasing extreme geometry-altering kits without verifying local legal bumper height limits. |

| Installation Phase | Having parts installed by a certified Automotive Service Excellence (ASE) technician and saving all diagnostic alignment sheets. | DIY installations involving cut springs, stacked lift blocks, or unauthorized frame welding. |

| Policy Update Phase | Adding a CPE endorsement and photographing all installed parts with visible date stamps. | Assuming a standard full-coverage policy automatically encompasses $5,000 in aftermarket upgrades. |

Taking these exact administrative steps ensures your vehicle remains protected, keeping your financial future as secure as your newly upgraded ride while you prepare for the next wave of industry regulations.

Navigating the Future of Modified Car Insurance

As vehicle technology continues to advance, the gap between factory engineering and aftermarket customization will only widen. Drivers must adapt to an era where modifying a car means modifying a complex, integrated safety network. By staying informed and communicating directly with your carrier, you can still enjoy the thrill of customization without risking financial ruin on the highway.

Actionable Next Steps

- Audit your current vehicle for any aftermarket parts installed by previous owners, particularly focusing on shocks, struts, and control arms.

- Review your Progressive Insurance policy declarations page specifically for the Custom Parts and Equipment clause limitations.

- Schedule a 15-minute call with your insurance agent to officially document any deviations from the factory build sheet using exact brand names and part numbers.

Staying ahead of these strict underwriting guidelines is the ultimate key to enjoying your custom build without sacrificing your peace of mind on the open road.