Many drivers adopted electric vehicles with the promise of near-zero maintenance and plummeting long-term ownership costs. For years, this compelling narrative held true, pushing millions to make the switch to America’s best-selling electric vehicle and revolutionizing the domestic auto market. Drivers enjoyed tax incentives, minimal charging costs, and a distinct lack of traditional mechanical failures like oil changes or transmission blowouts. However, a sudden, unprecedented shift in the auto insurance landscape has violently disrupted this financial honeymoon, catching thousands of drivers completely off guard and threatening to erase years of fuel savings in a matter of months.

Behind closed doors, leading actuaries and advanced collision repair specialists have identified a severe, systemic vulnerability that entirely contradicts everything we thought we knew about electric vehicle durability. A newly implemented manufacturing mandate has fundamentally altered how these specific vehicles absorb impact, triggering a massive, inescapable premium hike across the United States. If you own, lease, or plan to purchase a Tesla Model 3, understanding this hidden structural shift is no longer optional—it is the one key solution to your long-term financial survival and the only way to avoid catastrophic out-of-pocket expenses.

The Unrepairable Architecture: Why Premiums Are Skyrocketing

Studies prove that modern automotive manufacturing techniques increasingly prioritize assembly line speed and weight reduction over post-collision repairability. The core issue driving this crisis lies in the latest iteration of the vehicle’s structural battery pack. Instead of legacy modular designs—where individual power cells or small, defective modules could be easily isolated and swapped out—the new industry mandate pushes for a monolithic, unrepairable battery pack casing. This advanced engineering method brilliantly reduces overall vehicle weight and drastically cuts factory production costs, but it dangerously transfers immense financial risk directly onto the consumer.

| Driver Profile | Vehicle Generation | Direct Financial Impact & Policy Reaction |

|---|---|---|

| Early Adopters | Pre-Mandate Modular Models | Moderate baseline premiums, stable rate environments, and high carrier retention. |

| New Buyers | Post-Mandate Structural Models | Severe 43 percent rate hikes, heavily restricted carrier options, and forced high deductibles. |

| Lease Holders | Current Showroom Models | Mandatory gap insurance recalibrations, extreme liability risk, and strict lease return penalties. |

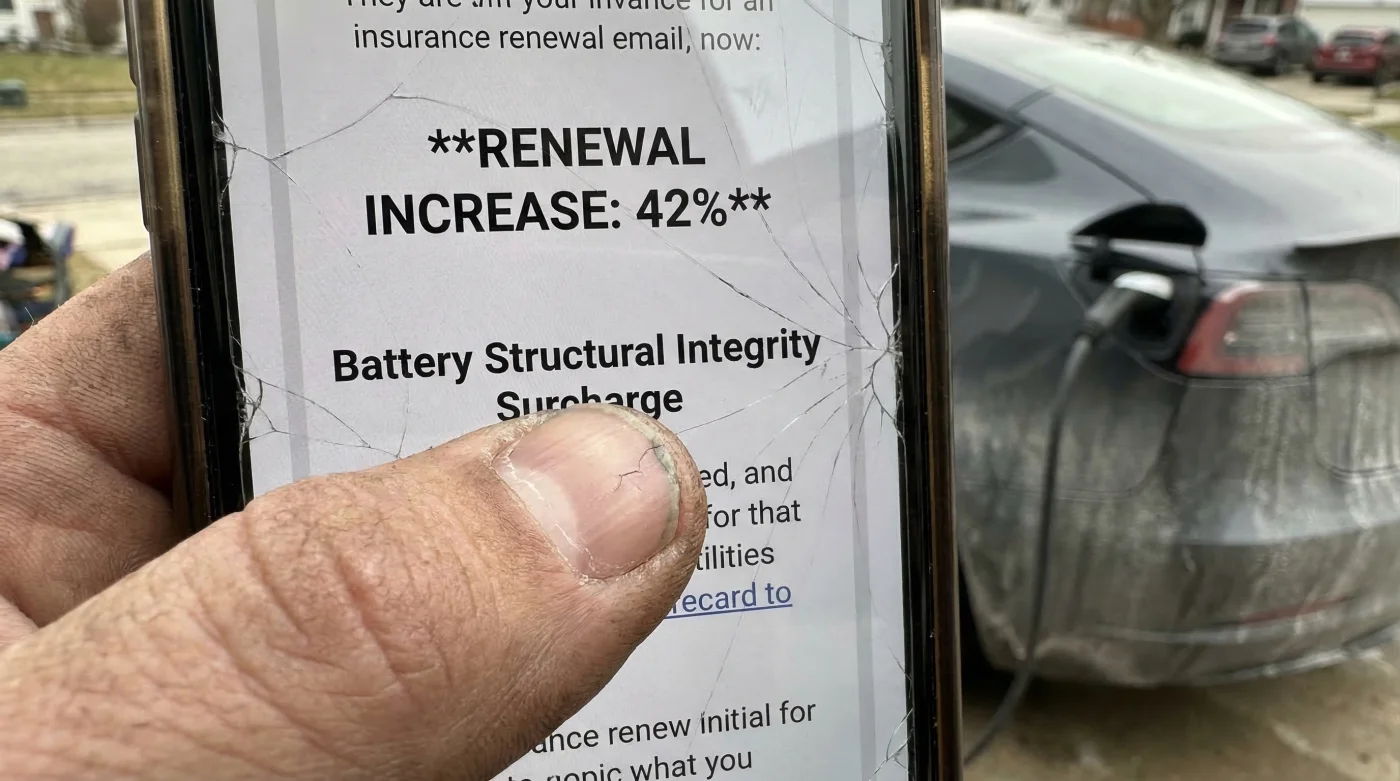

The 43 Percent Spike Explained

Insurance actuaries recently reported a staggering 43 percent spike in comprehensive and collision coverage costs specifically for these affected models. When a relatively minor fender bender or road debris impact scratches the underbelly of the vehicle, the lithium-ion structural casing cannot be safely inspected, patched, or certified for future road use. Because the battery casing also serves as a primary load-bearing component of the car’s frame, insurers are forced to assume catastrophic internal failure to avoid massive liability lawsuits.

- Symptom: Minor undercarriage scrape from a standard speed bump. Cause: Total battery replacement required due to strict, zero-tolerance structural integrity guidelines dictated by the manufacturer.

- Symptom: Skyrocketing monthly premiums immediately upon policy renewal. Cause: Insurance carriers aggressively pricing in the 100 percent total loss ratio on historically minor battery impacts.

- Symptom: Sudden carrier denial of comprehensive coverage in specific zip codes. Cause: Regional actuaries blacklisting specific VIN ranges due to unrepairable structural classifications and high regional accident rates.

To fully grasp why the nation’s largest insurers are panicking, we must look at the exact actuarial math dictating your new monthly bill.

The Actuarial Math: Decoding the Financial Damage

Experts advise that intimately understanding the raw underwriting data is your absolute best defense against unexpected, crippling repair bills. Major insurers utilize highly specific, algorithm-driven metrics to determine the risk-to-repair ratio for every vehicle on the road. With the modern Tesla Model 3, the traditional collision math has fundamentally inverted. The standard cost to replace a slightly compromised structural battery pack often exceeds 50 percent of the vehicle’s total actual cash value, automatically triggering a total loss designation under salvage laws in the majority of US states.

| Technical Repair Mechanism | Diagnostic Metric / Technology Used | Actuarial Dosing & Estimated Financial Cost |

|---|---|---|

| Modular Pack Repair (Legacy System) | Cell-level voltage testing and thermal imaging | $3,500 to $5,000 per isolated module swap. |

| Structural Casing Replacement (Mandate) | Ultrasonic resonance mapping and structural X-ray | $18,000 to $22,000 for a total factory pack swap. |

| Insurance Loss Ratio Recalibration | Average claim payout versus annual premium revenue | Catastrophic spike from 65 percent to over 105 percent. |

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

Strategic Coverage: Navigating the Premium Crisis

Despite the grim statistics, you are not entirely powerless against these sweeping rate hikes. By meticulously restructuring your insurance approach and understanding exactly what specific policy riders to demand from your broker, you can significantly mitigate the financial bleed. Standard, off-the-shelf automotive policies designed for internal combustion engines will leave you dangerously exposed to the high-tech nuances of the new structural battery mandates.

The Top 3 Insurance Adjustments for EV Owners

- 1. OEM Parts Endorsement: You must explicitly demand this rider to guarantee the use of Original Equipment Manufacturer casings. This prevents stingy insurers from legally forcing unsafe, aftermarket structural repairs that could void your warranty.

- 2. Battery-Specific Undercarriage Shielding Riders: Opt exclusively for progressive carriers that offer specialized, stand-alone riders for road debris damage to the lower battery plate, isolating these claims from your primary collision premium.

- 3. Agreed Value Coverage Restructuring: Shift immediately from standard Actual Cash Value (ACV) policies to Agreed Value coverage. This perfectly protects against the accelerated, artificial depreciation caused by widespread structural unrepairability reports.

| What to Look For (Premium Quality Guide) | What to Avoid (Financial Red Flags) |

|---|---|

| Carriers operating dedicated EV actuarial underwriting departments. | Generic, bundled policies that explicitly lump electric vehicles with traditional combustion vehicles. |

| Clear, legally binding definitions of ‘structural damage’ within the policy text. | Vague, open-ended clauses allowing the installation of ‘salvaged’ or ‘reconditioned’ battery replacements. |

| Riders specifically covering secondary thermal runaway risks post-collision. | Policies requiring third-party, non-certified damage appraisals from generalized local body shops. |

Armed with a scientifically sound insurance policy, you must also immediately implement hyper-aware daily driving habits to physically protect this highly sensitive structural component.

Defensive Driving for Structural Integrity

The single most effective way to permanently beat the insurance trap is to entirely avoid triggering a comprehensive claim in the first place. Because the monolithic casing architecture is incredibly susceptible to bottom-out damage and shear forces, altering your daily driving geometry is absolutely paramount. First, rigorously maintain a cold tire pressure of exactly 42 PSI to maximize crucial ground clearance and optimize battery efficiency. When operating in winter climates where temperatures drop below 32 degrees Fahrenheit, be hyper-vigilant of hidden ice chunks that act like concrete blocks against the undercarriage.

When approaching steep suburban driveways, aggressively crowned city roads, or unpaved shoulders, always enter at a deliberate 45-degree angle to completely prevent high-centering the heavy battery pack. Furthermore, strictly reduce your speed over parking lot speed bumps to strictly under 5 miles per hour. This precise speed control drastically prevents deep suspension compression from physically pushing the vulnerable structural battery casing down into the abrasive asphalt.

These small, highly actionable, daily adjustments act as an impenetrable physical insurance policy, safeguarding your wallet from the unseen engineering vulnerabilities literally sitting just inches beneath your feet.

The Future of EV Ownership Costs

The global automotive industry is currently trapped at a volatile crossroads between cutting-edge manufacturing efficiency and fundamental consumer repairability. While the latest Tesla Model 3 undoubtedly remains a marvel of modern American engineering and performance, this rigid new production mandate serves as a harsh, expensive reminder that rapid innovation often comes with severe hidden costs. Until third-party collision repair networks develop and deploy FAA-level non-destructive testing for complex structural batteries, insurance carriers will aggressively continue to default to totaling these slightly damaged vehicles.

To survive this transitionary period in automotive history, consumers must adapt their financial strategies immediately. Stay relentlessly vigilant, review your entire insurance policy meticulously at least every six months, carefully monitor your vehicle’s undercarriage for any signs of abrasion, and never blindly assume that a minor scrape is merely a cosmetic issue. The rules of vehicle ownership have permanently changed, and only the most educated drivers will avoid the devastating financial consequences.