Picture this: You have just spent four grueling hours at the local dealership. You have negotiated the price of your dream vehicle, completed the test drive, and finally, you are ushered into the dreaded back office to finalize the paperwork. Suddenly, the favorable financing terms you verbally agreed upon are mysteriously contingent on purchasing a $3,500 “ultimate protection package.” For decades, millions of American consumers have fallen victim to this psychological exhaustion tactic, quietly accepting inflated monthly payments and unwanted service plans just to get the keys and go home.

But an unprecedented institutional shift has just altered the auto industry’s landscape forever, effectively neutralizing the “hidden habit” of finance managers holding your loan hostage. A newly enacted federal safeguard specifically targets this predatory loophole, completely dismantling the standard practice of forced extended warranties for auto financing approval. By understanding this singular regulatory change, you can save thousands of dollars and legally force dealerships to honor your baseline financing without a single hidden add-on.

The Institutional Shift: Dismantling the F&I Office Trap

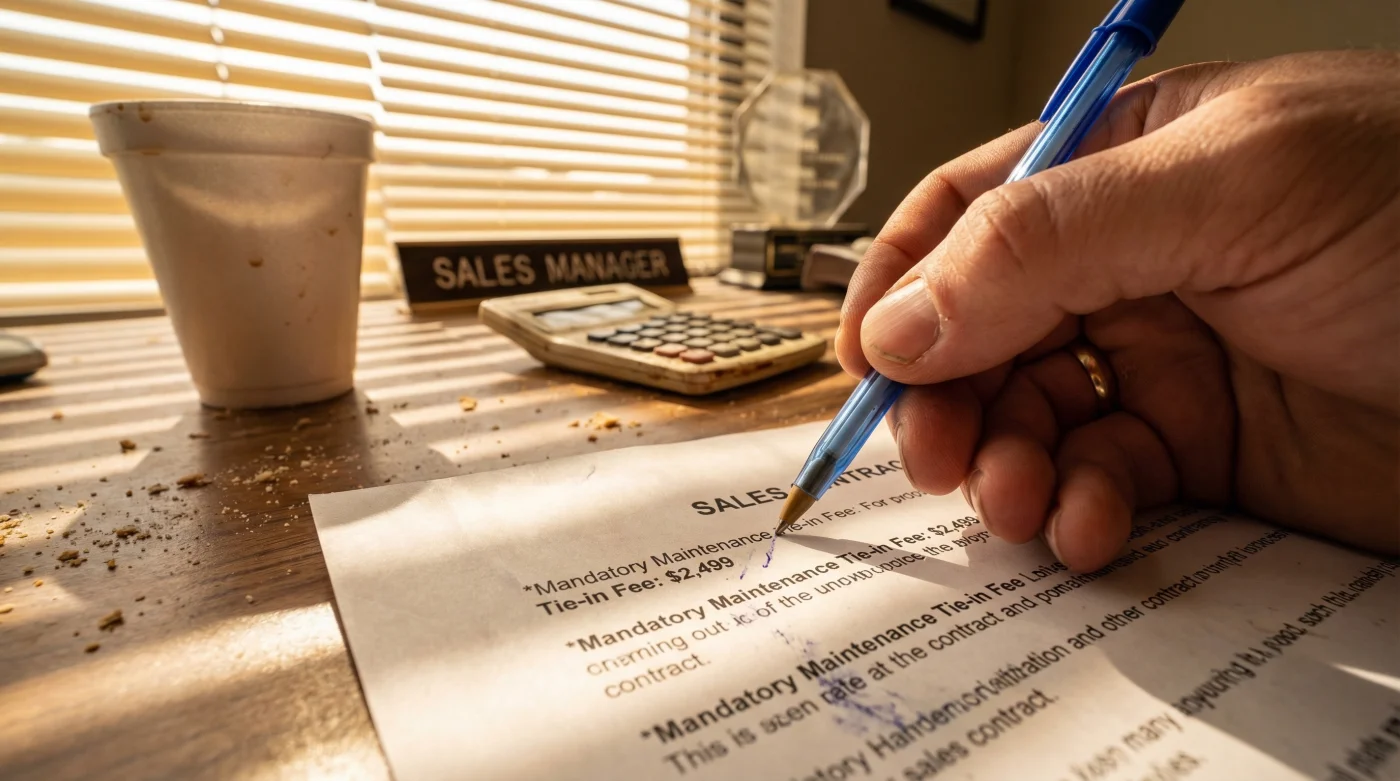

For years, the phrase caveat emptor (buyer beware) was the only defense consumers had against the opaque practices of the automotive Finance and Insurance (F&I) office. Dealerships routinely utilized tie-in sales, a deceptive strategy where the approval of a primary product (the auto loan) is illegally conditioned upon the purchase of a secondary product (a mandatory maintenance contract). Economic studies confirm that this singular tactic has siphoned billions of dollars annually from American households. The Federal Trade Commission has officially recognized this systemic abuse, bringing down the hammer on predatory dealership add-ons nationwide. Experts advise that consumers who actively assert their rights under these new guidelines immediately instantly remove the dealership’s leverage.

The Top 3 Impact Zones of the New Mandate

- Elimination of Bogus Fees: Dealers can no longer charge for add-ons that provide zero intrinsic value to the consumer, such as nitrogen-filled tires that were already installed.

- Separation of Financing and Products: Your creditworthiness dictates your loan approval, completely independent of whether you purchase service contracts.

- Mandatory Transparent Disclosures: Dealerships must provide an actual “Offering Price” that represents the full cash price of the vehicle minus government fees, entirely devoid of hidden backend charges.

| Consumer Profile | The Old Standard (Predatory) | The New FTC Reality (Protected) |

|---|---|---|

| Subprime Credit Buyers | Forced into $4,000 warranty to “appease the bank.” | Financing approved strictly on credit metrics; 0 mandatory add-ons. |

| First-Time Buyers | Subjected to exhaustion tactics and opaque bundling. | Receives clear, itemized “Offering Price” before F&I office entry. |

| Cash Buyers / Outside Financing | Denied service or charged arbitrary “market adjustment” fees. | Protected by anti-discrimination clauses enforcing baseline pricing. |

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

Decrypting the Mechanics of the CARS Rule

The core of this nationwide ban is driven by the Federal Trade Commission‘s sweeping Combating Auto Retail Scams (CARS) Rule. This framework specifically targets the narrative friction that occurs when consumers attempt to secure competitive auto financing. Under the CARS Rule, it is a direct federal violation for a dealership to imply that an extended warranty, gap insurance, or cosmetic protection plan is required to secure a lower Annual Percentage Rate (APR) or to get the loan funded at all. This practice, known in the industry as packing the payment, relies heavily on consumer ignorance regarding amortization and compound interest. By legally severing the tie between loan approval and F&I products, the CARS rule allows car buyers to confidently decline all dealer add-ons without facing any loan penalties or artificial rate hikes.

Diagnostic Checklist: Are You Being Targeted?

If you experience any of the following interactions on the showroom floor, you are likely facing a CARS Rule violation. Use this Symptom = Cause diagnostic guide to troubleshoot the negotiation:

- Symptom: The finance manager states, “The lender requires this service contract due to your credit score.” = Cause: Fraudulent tie-in coercion. Lenders do not require warranties for loan funding.

- Symptom: The contract is pre-printed with a $1,500 “Appearance Protection” fee that cannot be removed from the software. = Cause: Deceptive pricing omissions. All optional add-ons must be affirmatively selected by the consumer.

- Symptom: You are offered a 7% APR with the warranty, but a 9% APR if you decline it. = Cause: Illegal rate manipulation. The baseline buy-rate cannot be artificially inflated to punish the rejection of add-ons.

| Predatory Add-On Type | Average Cost | Amortized Cost (72 Months @ 8.5% APR) | Technical Legal Mechanism for Refusal |

|---|---|---|---|

| Mandatory Maintenance Contract | $3,500 | $4,482 (Adds $62/month) | CARS Rule: Prohibition of Tie-In Sales |

| VIN Etching / Security | $899 | $1,151 (Adds $16/month) | CARS Rule: Prohibition of Zero-Value Add-Ons |

| Paint/Fabric Protection | $1,200 | $1,536 (Adds $21/month) | CARS Rule: Affirmative Consent Mandate |

Once you understand the underlying mathematics of these predatory loans, the next crucial step is mastering the exact phrases and actions required to enforce your rights in the finance office.

Actionable Directives: Exercising Your New Federal Rights

Knowledge without execution is useless on the dealership floor. To actively benefit from the Federal Trade Commission ban, you must apply precise, actionable “dosing” to your negotiation strategy. Think of these metrics as your absolute boundaries. First, enforce a mandatory 24-hour review period on all final paperwork before signing. Second, demand exactly 1 itemized out-the-door price sheet that strictly separates the vehicle cost, taxes, registration, and optional products. Finally, maintain a strict limit of 0 mandatory add-ons. If a finance manager attempts to bundle a product, you must explicitly state: “I am declining all optional coverage under the provisions of the FTC CARS Rule. Please print the baseline financing contract.”

The Top 3 Negotiation Power-Moves

- The Pre-Emptive Strike: Email the sales manager before arriving, stating you are pre-approved and will not accept any F&I products. Have them acknowledge this in writing.

- The “Show Me the Bank Call” Tactic: If told the bank requires the warranty, request to conference call the lender’s underwriting department on speakerphone right then and there. The dealer will instantly backtrack.

- The Walk-Away Protocol: If the dealer refuses to remove the mandatory maintenance contract, physically stand up. The sheer threat of losing a funded deal over an illegal add-on usually triggers immediate compliance.

| Dealership Quality Indicator | What to Look For (Lawful Progression) | What to Avoid (Red Flags) |

|---|---|---|

| Pricing Transparency | Clear “Offering Price” prominently displayed online and in-store. | Prices that include “assumed” down payments or mandatory rebates you don’t qualify for. |

| F&I Office Conduct | Menu-style presentation where you must manually initial to accept products. | Pre-filled contracts with checked boxes for ancillary products. |

| Financing Independence | Loan rate is negotiated and locked prior to discussing warranties. | Rate suddenly changes or “lender approval” drops when you decline the warranty. |

By utilizing this quality guide to vet your dealership, you permanently shield yourself from predatory practices and secure a fair, transparent automotive investment.