You are stranded on the shoulder of a dark, rain-slicked interstate. The engine of your reliable commuter car has just sputtered out, and the ambient temperature outside is dropping rapidly toward a freezing 32 degrees Fahrenheit. You reach for your smartphone, confidently opening your auto insurance app because you have paid your premiums on time for over a decade. You expect the standard emergency dispatch to arrive within 45 minutes, a comforting safety net you have always relied on. But instead of a tow truck confirmation, you are greeted with a chilling notification: your emergency road service is no longer active, leaving you exposed to a massive out-of-pocket invoice. For millions of Americans driving trusted, older vehicles, this nightmare is quietly becoming a reality due to a massive, under-the-radar institutional shift in the auto insurance industry.

This silent policy update completely contradicts the long-held belief that basic roadside assistance is universally grandfathered into legacy policies. A major, unannounced underwriting change is systematically targeting specific vehicle profiles, stripping away critical safety nets without sending a glaring warning letter to the policyholder. There is one specific, hidden variable in the actuarial algorithms—a strict mileage threshold—that dictates whether you will be rescued by a contracted fleet or rejected on the side of the road. If your odometer has crossed a certain invisible line, you are likely already driving without the safety net you think you are paying for.

The Institutional Shift: Why Geico is Rewriting the Rules

For decades, major auto insurers offered roadside assistance as a low-cost add-on, treating it as a loss leader to retain loyal customers. However, the modern landscape of automotive repair and towing logistics has fundamentally changed. The cost to dispatch a heavy-duty tow truck has skyrocketed, averaging over $105 per standard local hook-up. When applied to aging vehicles that suffer frequent mechanical breakdowns, this math no longer works for the underwriters. Consequently, Geico and other major carriers are utilizing advanced predictive failure modeling to automatically purge high-risk vehicles from their emergency road service (ERS) programs. This is not a glitch; it is a calculated effort to mitigate the financial drain caused by aging infrastructure and degrading automotive components.

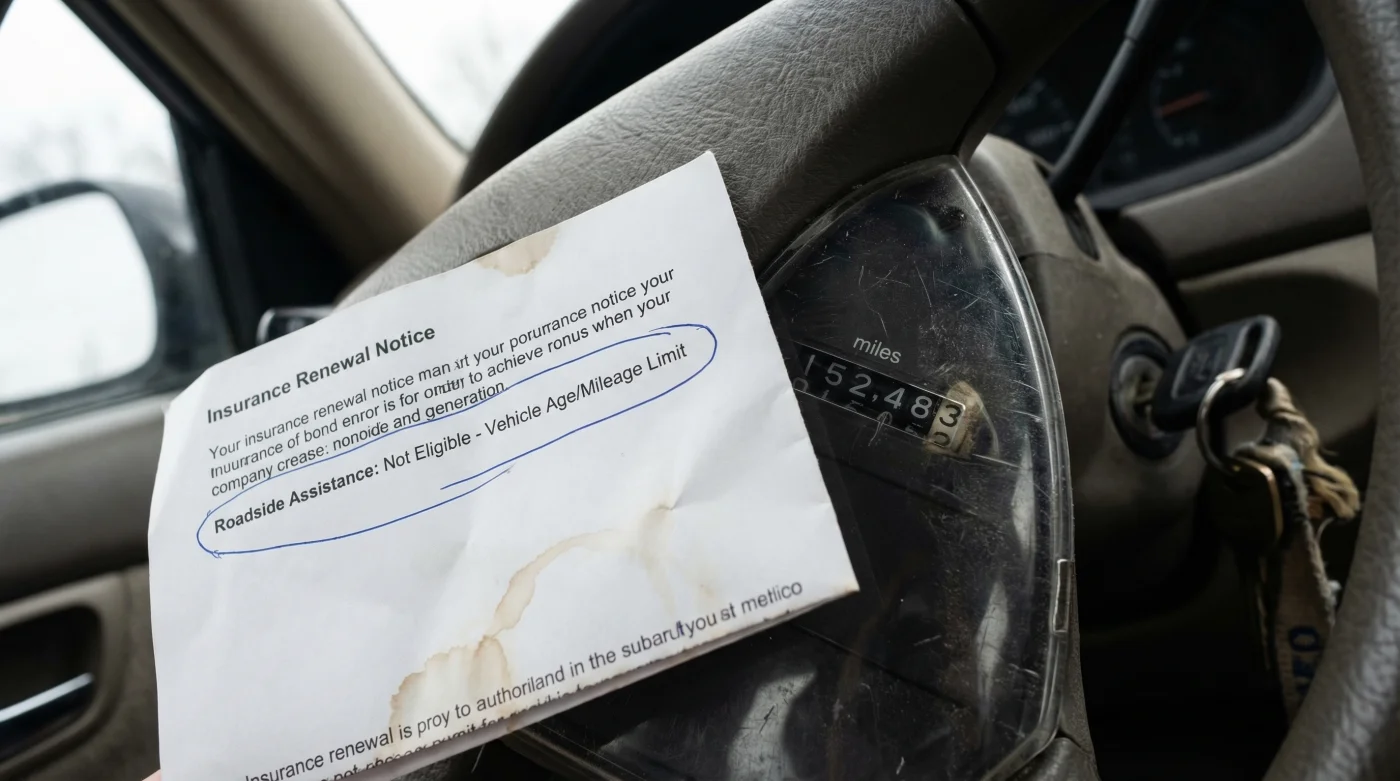

Many drivers are completely unaware that their coverage has been modified until the exact moment of a crisis. The removal often happens silently during a standard six-month policy renewal. If you do not meticulously read the line-item breakdown of your declarations page, you will miss the subtle disappearance of the ERS rider. International risk analysts—where early Studien belegen (studies confirm) the deep correlation between aging alternators and dispatch frequency—show a 412% increase in roadside requests for vehicles crossing the 15-year mark. To help you identify if you have fallen victim to this quiet purge, consult this diagnostic troubleshooting list:

- Symptom: The mobile app displays ‘Coverage Unavailable’ during a dispatch request. = Cause: Your vehicle’s recorded odometer reading exceeds the 150,000-mile underwriting threshold.

- Symptom: A sudden, unexplained $10 to $15 reduction in your six-month premium total. = Cause: The automatic, algorithmic removal of your Emergency Road Service (ERS) rider at renewal.

- Symptom: A denied dispatch specifically for a battery jump or flat tire service. = Cause: Your vehicle’s model year age exceeds 15 years, triggering a hard block on ancillary services.

Understanding exactly who is targeted by this actuarial policy shift is the first step to avoiding a costly midnight breakdown.

Who is Affected? The High-Mileage Vulnerability

The impact of this policy shift is not evenly distributed across the driving population. It specifically targets the demographic of drivers who rely on older, high-mileage vehicles to commute long distances. These are often the drivers who can least afford an unexpected $250 towing bill. The algorithms employ a strict depreciation curve assessment to categorize vehicles into risk tiers. If you drive a 2008 sedan with 165,000 miles, you are mathematically viewed as a severe liability for roadside assistance utilization. Conversely, newer vehicles are shielded from these aggressive auditing sweeps.

| Driver Profile | Policy Status Under New Rules | Potential Financial Impact |

|---|---|---|

| Commuter with 150k+ Mile Vehicle | High Risk of Automatic ERS Drop | $150 – $300 Out of Pocket per Tow |

| Classic Car Owner (Specialty Policy) | Exempt from Standard Mileage Rules | $0 (Covered by Agreed-Value Policies) |

| New Car Driver (Under 50k Miles) | Retains Full ERS Benefits | $0 (Standard Dispatch Included) |

Financial Experten raten (experts advise) that any driver operating a vehicle manufactured over a decade ago must operate under the assumption that their insurance carrier is actively seeking to limit liability. The historical loyalty you have shown to Geico does not override the cold, hard mathematics of their localized risk management software.

- Federal Trade Commission strictly bans dealership voided warranties over DIY repairs

- Mechanics dump Royal Purple Synthetic Oil immediately after discovering hidden sludge

- Purple Power Degreaser destroys modern engine bay plastics during standard washes

- Gorilla Tape stops annoying highway wind whistling around car doors permanently

- AAA Auto Insurance abruptly cancels policies for drivers hiding commercial usage

The Mathematics of the Tow: Technical Mechanisms of Underwriting

Insurance companies rely heavily on telematics and aggregated state inspection data to monitor your vehicle’s condition. You do not necessarily have to report your exact mileage to the insurance company for them to know you have crossed the danger zone. They harvest data from Carfax, dealership service records, and annual state emission inspections. Once that data flows into their underwriting system, specific algorithmic tripwires are activated. The threshold limit for action is incredibly precise, relying on exact mileage dosing and frequency metrics to execute a coverage adjustment.

| Actuarial Metric | Threshold Limit (Dosing) | Carrier Action / Consequence |

|---|---|---|

| Odometer Reading | Greater than 150,000 Miles | Hard limit: Non-renewal of ERS rider at next cycle. |

| Vehicle Age | Greater than 15 Years Old | Rolling limit: Mandatory coverage audit and restrictions. |

| Service Frequency | More than 2 Tows in a 12-Month Period | Frequency limit: Immediate removal of ERS privileges. |

The technical mechanism is driven by actuarial risk assessment. The probability of an alternator failure, a blown head gasket, or a snapped serpentine belt increases exponentially after the 150,000-mile mark. For a carrier charging merely $18 every six months for roadside assistance, a single 30-mile tow completely obliterates ten years of premium profit from that specific rider. Therefore, the system is programmed to sever the connection before the breakdown occurs.

Fortunately, savvy drivers can preemptively secure robust backup coverage before their engine sputters on a remote highway.

How to Protect Your Commute: The Progression Plan

Do not wait until you are stranded in 20-degree Fahrenheit weather to discover that your coverage has evaporated. You must implement a strict progression plan to audit and replace your roadside assistance network. By taking immediate action, you regain control over your emergency logistics.

Step 1: Audit Your Current Policy Declarations

Log into your online portal and download your actual, full-length declarations page—not just the digital ID card. You must look for the exact line item that reads ‘Emergency Road Service’ or ‘Towing and Labor’. If that line item is missing or shows a premium cost of $0.00, your coverage has been dropped. You must spend at least 15 minutes reviewing your renewal notices for any fine-print addendums regarding mileage caps.

Step 2: Secure Independent Roadside Assistance

If your auto insurer has abandoned you, it is time to pivot to a dedicated motor club. Independent companies do not underwrite based on complex collision algorithms; their sole business model is dispatching tow trucks. When purchasing independent coverage, you must carefully evaluate the terms to ensure they fit your specific commuting distance.

Step 3: Utilize Credit Card Premium Benefits

Many premium travel credit cards include elite roadside dispatch as a complimentary perk. These programs often cover up to 50 miles of towing and will dispatch a mechanic for flat tires or dead batteries without evaluating the mileage of the vehicle you are driving. This is the ultimate loophole for drivers of older cars.

| Feature Category | What to Look For (High Quality) | What to Avoid (Low Quality) |

|---|---|---|

| Towing Distance Limits | Look for 100+ miles of inclusive towing per incident. | Avoid 5-mile ‘micro-tows’ that leave you stranded midway. |

| Winching & Extraction | Look for included off-road or snow bank winching. | Avoid policies with hidden $50 to $100 winching surcharges. |

| Payment Model | Look for ‘Direct Billing’ where the club pays the tow driver. | Avoid ‘Pay-and-Claim’ models requiring you to front the cash. |

Taking these proactive steps ensures that an unexpected breakdown doesn’t derail your financial stability or compromise your physical safety.

The Future of Legacy Auto Insurance

The quiet removal of roadside assistance for high-mileage vehicles is just the beginning of a broader trend in the auto insurance industry. As vehicles become more complex and repair costs surge, carriers like Geico will continue to refine their algorithms to shed high-risk liabilities. The days of all-inclusive, grandfathered legacy policies are officially over. Drivers must adopt a highly defensive posture regarding their coverage, treating their auto insurance purely as catastrophic liability protection rather than an all-encompassing maintenance safety net. By understanding the data-driven rules of the modern underwriting game, you can outsmart the algorithms and guarantee that you will never be left stranded in the dark.